Kalshi just closed a $1 billion funding round at an $11 billion valuation. Polymarket processed over $1 billion in a single month by late 2025. And neither platform takes the other side of a single bet.

That’s the part most founders misread when they first look at this space. This isn’t a sportsbook with better branding. Prediction market platforms are exchanges — they collect fees on every trade regardless of which outcome wins, build liquidity networks, and in the best cases stack four or five revenue layers on top of the base fee engine.

In 2026, the sector is real enough to attract institutional capital and complex enough that founders who don’t understand the revenue mechanics will overpay for infrastructure and undercharge on the things that actually matter.

Why 2026 Is a Different Market

Most of what was written about prediction market monetization in 2021 or 2022 was theoretical. Volume was thin, most platforms operated offshore, and regulators were hostile.

That’s not the situation now. Kalshi hit $50 billion in annualized volume in 2025, up from $300 million the prior year — a roughly 16x jump in 12 months. The Super Bowl alone cleared $1 billion on their platform. Polymarket completed a US relaunch through its acquisition of QCEX, a licensed derivatives exchange, and is actively rolling out to American users as of March 2026.

Regulatory clarity is the biggest unlock. When Kalshi won its legal fight against the CFTC, it didn’t just survive — it got designated as a contract market. That designation is now a trust moat. Institutional liquidity providers and serious traders don’t participate on platforms without it. If you’re building something intended to scale beyond crypto natives, regulatory status isn’t optional.

So. Non-regulated platforms aren’t automatically dead. Plenty run profitably targeting crypto users comfortable with offshore USDC-settled contracts. But the ceiling is lower, the banking relationships are harder, and you can’t list the high-volume financial event contracts — Fed rate decisions, CPI prints, earnings — that are driving Kalshi’s growth. The choice between regulated and unregulated isn’t a moral one. It’s a product decision with specific revenue consequences.

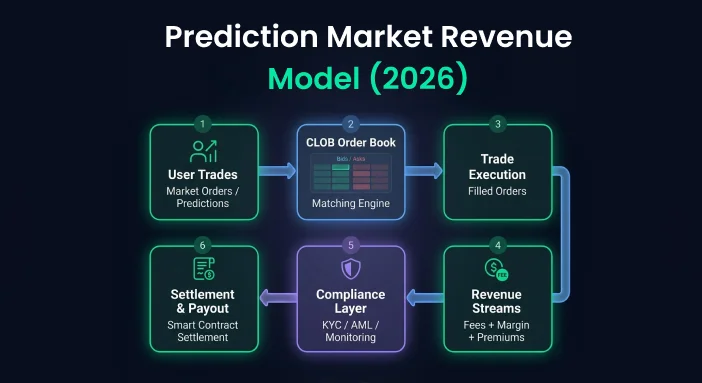

The Core Revenue Engine: Trading Fees on a CLOB

The foundation of every prediction market business model is the trading fee. Platforms charge a percentage of contract value, collected at settlement or at trade execution depending on the architecture.

Kalshi takes its fee at settlement — if you buy a YES contract at $0.60 and it resolves YES, the platform takes roughly 1–2% of your payout before it hits your wallet. Polymarket runs a CLOB (Central Limit Order Book) on Polygon, with fees baked into the order matching layer. The math is direct: $100 million in monthly volume at a 1% average fee rate is $1 million per month. At Kalshi’s current annualized volume, fee revenue alone explains their $1.5 billion revenue figure.

This is the same model as the NYSE or NASDAQ. The exchange doesn’t care who wins. It cares about volume. Everything else in your platform — liquidity incentives, market variety, UX quality, API access for automated traders — is ultimately in service of driving more trades through the fee engine.

For founders starting out, don’t build a fee structure that discourages trading. One team priced their take-rate at 4% upfront and thought they were being clever about margin. Volume dried up by month two because arbitrage traders walked the moment the math stopped working for them. Start at 1–2%, earn the volume first, then test fee sensitivity.

If you’re looking to launch your own exchange with a configurable fee engine, prediction market clone script setups handle this architecture out of the box — including CLOB order matching, settlement logic, and liquidity provider tooling.

Spread Revenue and Market Making Economics

Some platforms skip direct trading fees and earn through bid-ask spreads instead. If a contract trades at $0.48 bid and $0.52 ask, that $0.04 differential is spread revenue — captured by whoever is posting liquidity on the other side.

Platforms can earn this directly by acting as market makers on thinly traded events, or they can structure revenue-sharing arrangements with designated market makers (DMMs) who post liquidity in exchange for a cut of the spread. Polymarket uses the latter approach. DMMs provide depth, spreads narrow over time, and the platform benefits from the higher volume that tighter pricing creates.

But there’s a real structural risk here: adverse selection. When an informed trader knows an outcome is 90% likely but the market shows 55%, they’ll hit every available ask until inventory is gone. The market maker absorbs the loss. Managing this requires circuit breakers, automatic quote skewing as position inventory accumulates, and hard position limits per market. Budget at minimum $15,000–$30,000 for market making risk tooling if your platform plans to act as a DMM on any event category with real news sensitivity.

Four Revenue Layers Founders Usually Ignore

Most platforms stop at fees and spreads. The ones scaling past $10M ARR are building these on top.

Data API licensing. Prediction market probabilities are crowd intelligence in real time. Banks, hedge funds, political campaigns, and media organizations pay for clean API access to this data. Institutional licensing starts around $5,000 per month and scales with query volume. Most platforms haven’t gotten here yet, which means there’s still first-mover room.

Subscription and SaaS tiers. A market analytics dashboard, automated reporting, custom market creation tools, and embeddable prediction widgets convert well on monthly plans. This works especially well for B2B customers — research firms, consulting shops, or enterprise clients running internal forecasting programs.

Market listing fees. Brands and organizations pay to create sponsored prediction markets. A pharmaceutical company running an FDA approval market for investor relations, or a media company hosting branded entertainment predictions, will pay $2,000–$10,000 for listing and promotion depending on expected volume. It also drives organic user acquisition at near-zero marginal cost.

Tokenomics. If you’re building on Web3 infrastructure — Polygon, Base, Arbitrum — a governance token creates a fourth revenue layer through staking rewards, LP incentive pools, and treasury yield. For a new platform targeting crypto-native users, token design done right can fund your liquidity bootstrapping phase without diluting equity. Just don’t design it as a profit-sharing mechanism if you’re anywhere near the US market.

Regulatory Reality in 2026

Getting CFTC designation as a contract market costs real money. Legal fees, compliance infrastructure, and the application process run $500,000 to $2 million before approval. That’s not an early-stage investment.

But the return is real. US users, institutional liquidity providers who won’t touch non-regulated venues, banking relationships for fiat on/off ramps, and access to financial event contracts that drive Kalshi’s $11 billion valuation. You can’t legally list “Will the Fed cut rates in June?” without it.

Polymarket’s path was acquisition rather than direct application — buying QCEX instead of going through the full licensing process from scratch. If you’re a well-funded team targeting the US market, that approach is worth modeling. If you’re earlier stage and focused on global crypto users, operating offshore with USDC settlement may be the right call for 18–24 months, with regulatory expansion as a later-stage milestone.

What you can’t do is ignore compliance entirely and assume goodwill. The CFTC has shown it will act, and the cost of enforcement is higher than the cost of compliance.

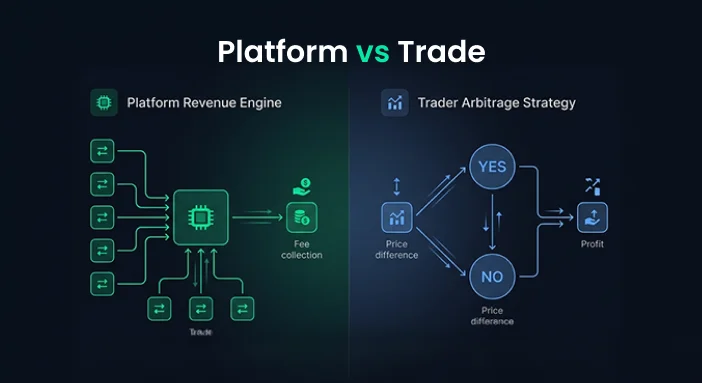

Platform vs Trader: Two Ways to Make Money in This Space

The business model conversation splits here depending on whether you’re building a platform or trading on one.

For platforms: revenue compounds with volume. Recurring fee income, growing API subscriptions, and expanding market inventory layer on each other in a way that resembles SaaS more than gambling. Platform revenue is structural and grows regardless of who wins which bet.

For traders: the game is different. The people making consistent money in prediction markets in 2026 aren’t predicting outcomes better than the crowd. They’re finding structural mispricings the market hasn’t corrected yet. Polymarket’s price oracle for short-duration crypto markets runs a 2–5 second lag behind actual exchange data. Informed participants running automated systems have turned that gap into six-figure returns. One former NOAA systems developer built a weather market bot that exploited the window between new GFS forecast releases and Polymarket’s pricing update cycle — turning $1,000 into $79,000.

Domain expertise also compounds in ways pure capital doesn’t. A healthcare analyst trading FDA approval markets, a political scientist on election contracts, or a macro trader specializing in Fed decisions — these people have calibration advantages retail participants can’t replicate quickly. The Kelly Criterion is the standard framework for position sizing: bet a fraction of your bankroll proportional to your edge, and keep positions sized so a losing streak doesn’t wipe you out before the edge shows up.

Most early traders fail because they treat prediction markets like a news-based guessing game. The professionals treating it like an information arbitrage business are the ones extracting consistent profit.

Risk Factors That Sink Platforms Early

Three things catch founders off guard consistently.

Insider trading exposure. In early 2026, six accounts on Polymarket placed large YES bets on “US strikes Iran by February 28, 2026?” and cleared over $1.2 million in profit before the strikes happened. The timing raised clear insider trading concerns. As a platform operator, you’re not automatically liable for user conduct — but the reputational damage is yours, and regulators are watching. Build KYC, position monitoring, and unusual activity flags into the platform from day one, not after the first headline.

Tax friction for users. Kalshi and PredictIt issue 1099-MISC forms listing net profits as ordinary income. For US users, prediction market winnings get taxed at the same rate as wages — no capital gains treatment. This creates real friction at tax time and becomes a support burden fast. Build in-app tax summaries and P&L exports before you need them.

Adverse selection at scale. As your platform grows, you’ll attract smarter traders. Smarter traders pick off mispriced markets faster than your liquidity providers can reprice. If you don’t have strong market-making infrastructure and dynamic spread tooling in place, liquidity providers pull out, spreads widen, volume drops, and the fee engine stalls. This is the spiral that kills second-year platforms. Build the risk tooling early, not reactively.

Frequently Asked Questions

How do prediction market platforms make money without taking bets?

They act as exchanges, not bookmakers. Platforms collect fees on every trade or capture bid-ask spreads, earning revenue from volume rather than outcomes. The more trades executed, the more revenue the platform generates — regardless of which side wins. This is structurally identical to how stock exchanges make money.

What’s the typical fee structure for a prediction market platform in 2026?

Most platforms charge 1–2% of contract value, taken at settlement or execution. Some use a maker/taker model similar to crypto exchanges — around 0.1–0.5% per side. The key variable is whether you charge at trade entry or at settlement, which affects how users perceive the cost and how you model revenue on unresolved contracts.

How much does CFTC regulation cost to obtain?

Realistically, $500,000 to $2 million in legal, compliance infrastructure, and application costs before approval. Kalshi spent years on this process. The alternative is acquiring a licensed entity, which is how Polymarket returned to the US market.

Is prediction market income taxed as ordinary income?

Yes, at least for US users currently. Platforms like Kalshi and PredictIt issue 1099-MISC forms with net profits listed as ordinary income, taxed at the same rate as wages. There’s no capital gains treatment as of 2026, though the tax framework is still evolving.

What is adverse selection and why does it matter for platform operators?

Adverse selection happens when informed traders consistently trade against less-informed liquidity providers. A market maker posting quotes on a court ruling market loses badly if someone with early access to the decision takes every available position. Managing it requires position limits, dynamic spread widening, and event-triggered quote withdrawal — it’s the main reason small platforms bleed liquidity as they grow.

Can tokenomics work as a primary revenue stream?

Not as a primary stream, but as a meaningful secondary one. Governance tokens, staking rewards, and LP incentive pools work well for Web3-native platforms targeting crypto users. In the US market, any token structure that resembles profit-sharing attracts securities scrutiny. Design for utility and governance, not yield distribution.

How does a white label prediction market generate revenue for the operator?

White label platforms typically charge $20,000–$80,000 upfront for licensing, plus a monthly platform fee and optional revenue sharing on transaction volume. Operators apply their own fee structures to end users on top of that. The provider earns regardless of operator performance, which makes it a relatively stable SaaS-adjacent model for both sides.