The CFTC made it official on March 31, 2026. Enforcement Director David Miller named willful AML and KYC violations as one of five agency priority areas — right alongside insider trading and market manipulation — and flagged criminal referrals as a real option for deliberate non-compliance. One founder we know launched an offshore prediction platform with “KYC coming soon” on the roadmap. Trading engine worked. UI was clean. Payment processors dropped them 90 days after launch following a routine compliance review. The rebuild cost $90,000 and seven months. Compliance isn’t a phase 2 feature. It’s what keeps the platform alive.

Why the Compliance Stakes Jumped in 2026

Polymarket paid a $1.4 million CFTC settlement in 2022 for running an unregistered derivatives platform without KYC controls. The fix? It spent $112 million acquiring licensed exchange QCX just to re-enter the US market properly. That’s a steep correction for skipping compliance at the start.

The regulatory shift accelerated after the 2024 US election cycle drove record prediction market volume. Both the CFTC and FinCEN are actively watching this space. FATF’s updated Recommendation 15 explicitly covers VASPs running crypto-enabled prediction markets, with Travel Rule obligations applying to transfers above $3,000. The global RegTech market passed $22 billion in mid-2025, growing at about 23.5% annually, because compliance infrastructure is now a baseline expectation, not a differentiator.

There’s also a risk that has nothing to do with regulators. Payment processors run automated compliance reviews. One pattern of suspicious transaction activity is enough to trigger a deactivation notice, not a warning. Platforms without transaction monitoring lose banking relationships faster than they lose traders.

And the risk isn’t only external. Without identity verification, your platform becomes attractive to fraudsters running account-level layering schemes: multiple accounts, small deposits, coordinated trading on both sides of a contract, then fast withdrawal. It’s a documented pattern on event contract platforms that skip AML monitoring. You may never see a CFTC enforcement action, but you’ll see chargebacks, frozen accounts, and payment processor flags long before that.

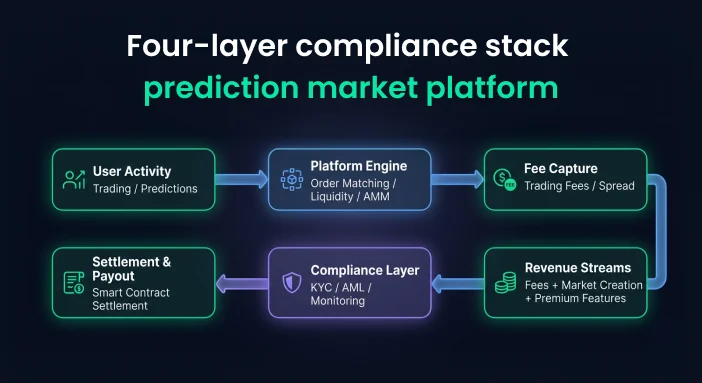

The Four Layers Your Compliance Stack Needs

Most founders treat KYC and AML as a single toggle in the admin panel. They’re not. A properly built compliance stack for a white-label prediction market software has four interdependent layers. Skip one and the others don’t hold.

Layer 1: Identity verification at onboarding. This is eKYC — collecting government-issued ID, running biometric liveness detection, and matching selfie to document. No user deposits, trades, or withdraws until this step completes and passes.

Layer 2: Risk-based customer due diligence (CDD). After identity verification, every account gets a risk score. Low-risk users pass through standard CDD. High-risk accounts — flagged by jurisdiction, account type, or initial transaction pattern — go through Enhanced Due Diligence (EDD): additional documentation, source-of-funds declarations, manual review, and quarterly re-assessment.

Layer 3: Ongoing transaction monitoring. Every deposit, bet, withdrawal, and internal transfer runs through a rule engine watching for structuring behavior, wash trading, layering, and velocity anomalies.

Layer 4: Perpetual KYC (pKYC). Compliance doesn’t end at onboarding. pKYC re-verifies accounts when risk signals change — new jurisdiction login, abnormal withdrawal volume in a short window, significant behavior shift, or deposits crossing cumulative $10,000 in 30 days.

Build all four before launch. Adding them retroactively costs 3 to 5 times more in engineering time and typically requires a full user data migration. One team we worked with tried to bolt on transaction monitoring post-launch — they had to re-onboard 4,200 existing users because their original data capture didn’t include the fields their AML system needed.

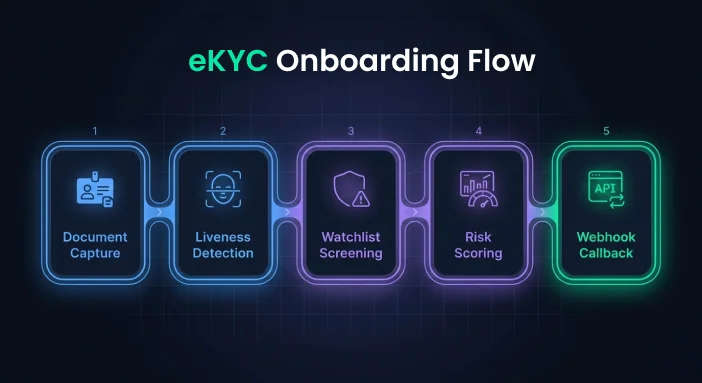

eKYC Onboarding: What the Flow Actually Looks Like

The eKYC flow in a prediction market clone script has five steps. Understanding each matters because each one is a potential drop-off point, and compliance vendors differ significantly in how they handle each.

Step 1: Document capture. The user photographs a government-issued ID — passport, driver’s license, or national ID card. The SDK auto-crops, corrects skew, and runs OCR to extract name, date of birth, document number, and expiry. Most modern SDKs handle this client-side before upload to reduce latency.

Step 2: Biometric liveness detection. The user takes a selfie or records a short video clip. The liveness check confirms it’s a real person, not a photograph or silicone mask, then runs a face match between the selfie and the captured ID document. This is where synthetic identity attempts fail. Sumsub’s passive liveness detection rejects synthetic fraud attempts at roughly 95% accuracy in production environments, based on their published benchmarks.

Step 3: Watchlist and sanctions screening. The extracted identity data runs against OFAC SDN lists, global PEP registries, Interpol notices, and jurisdiction-specific watchlists in real time. Response time is 3 to 8 seconds for most tier-1 KYC providers when API latency is healthy.

Step 4: Risk scoring. The system assigns a risk tier based on nationality, document type, IP geolocation, and any watchlist flags. Score thresholds determine auto-approval, manual review queue, or rejection.

Step 5: Webhook callback to your backend. The KYC provider posts the result to your platform. Your system updates the user’s verification status, unlocks trading features, and writes the result to your audit log with an immutable timestamp.

In a Laravel backend, this integrates cleanly through queue workers that handle webhook events asynchronously without blocking the main request cycle. In Node.js, you’d run a dedicated compliance microservice on a separate port with its own database connection, processing events and emitting status changes to the trading service via RabbitMQ or Kafka. Keeping compliance logic in its own service means you can swap KYC providers without touching your trading engine — which matters when FATF requirements update and your current provider doesn’t keep pace. For a broader look at how the full platform architecture fits together, see our guide on how to build a prediction market platform.

AML Transaction Monitoring and SAR Filing

This is the part most prediction market clone scripts handle worst. They list “AML monitoring” on the features page and ship a basic spend threshold alert. That’s not AML monitoring. That’s a receipt printer.

Real AML transaction monitoring on an event contract trading platform watches for specific behavioral patterns. Structuring: multiple deposits just under $10,000 — say, $9,700 then $9,400 in the same week — to avoid FinCEN reporting thresholds. Wash trading: placing opposing bets on the same contract across two user accounts to simulate volume or extract value. Velocity anomalies: 40 trades across 12 different markets in 6 hours followed by a full withdrawal. And cross-account clustering: multiple accounts sharing device fingerprints, email domains, or IP subnets that behave in coordinated patterns.

Your rule engine needs at minimum a dozen configurable rules at launch. Build them on top of providers like Sardine or Chainalysis for blockchain analytics, then layer custom rules for fiat transaction patterns. Chainalysis Reactor traces on-chain fund flow and flags wallets connected to known darknet markets or sanctioned addresses — essential if your platform accepts USDC or ETH deposits.

When a transaction triggers a suspicious flag, the workflow goes: freeze the transaction, notify the compliance queue, analyst reviews within 24 to 72 hours, then either clear the flag or escalate to a Suspicious Activity Report (SAR). In the US, SARs file through FinCEN’s BSA E-Filing portal. You’re required to file within 30 days of detecting suspicious activity. You cannot notify the user they’ve been reported — that’s called tipping off, and it carries its own penalties under 31 U.S.C. § 5318(g)(2).

Build SAR filing into your admin dashboard from day one. The FinCEN portal integration isn’t trivial. One platform we know tried to add it retroactively and spent three weeks getting the XML schema right for their first manual filing.

OFAC Screening, PEP Checks, and Geo-Restrictions

OFAC sanctions screening runs at two points: during onboarding and on every transaction. The onboarding check confirms the user doesn’t appear on any OFAC Specially Designated Nationals (SDN) or Blocked Persons list. The transaction-level check fires every time funds move.

PEP screening catches politically exposed persons — current or former government officials, close family members, and known associates. PEPs don’t get rejected automatically. They get flagged for EDD. You collect source-of-wealth documentation, apply heightened monitoring, and review quarterly instead of annually. Failing to apply EDD to a PEP account is one of the more common AML audit findings for fintech platforms and shows up consistently in enforcement actions.

Geo-restrictions need IP-layer enforcement, not just a registration form checkbox. Block at the CDN level using Cloudflare’s geo-IP rules or your load balancer’s access controls — users in restricted jurisdictions shouldn’t even load your registration page. Build a lightweight geo-check API endpoint that the frontend pings before rendering any onboarding assets.

High-risk jurisdictions for a US-targeted prediction market include North Korea, Iran, Cuba, Syria, and any country on the current FATF grey or black list. That list updates every six months, so your geo-block rules must be configurable from the admin panel without a code deploy. Hardcoding jurisdiction blocks into the application creates compliance debt every time FATF publishes an update.

Travel Rule Compliance for Crypto Prediction Markets

If your prediction market clone script accepts crypto deposits, FATF’s Travel Rule applies. It requires that any crypto transfer above $3,000 — or $1,000 in jurisdictions like Singapore and the EU — includes verified originator and beneficiary data transmitted alongside the transaction itself. This isn’t optional for VASPs. It’s a FATF Recommendation 16 obligation that most major jurisdictions have codified into national law.

In practice, this means adding a Travel Rule middleware layer between your crypto wallet module and your compliance database. The main providers are Notabene, Sygna Bridge, and VerifyVASP. When a user initiates a crypto withdrawal, your system identifies the receiving VASP, checks if they’re a registered counterparty in the Travel Rule network, and transmits originator and beneficiary data fields in real time.

If the receiving VASP isn’t in the network, hold the transaction and prompt the user for additional documentation before releasing the funds. That pause in the UX is not a flaw. It’s the compliance control working as designed.

Don’t assume stablecoins get a pass. Travel Rule obligations apply to USDC, USDT, and DAI transfers the same way they apply to BTC or ETH. Several prediction market operators learned this when they accepted USDT deposits without a Travel Rule solution in place and received FATF compliance notices from their banking partners.

Beneficial ownership verification also matters here. When a corporate account registers as a trader on your platform, you’re expected to identify any individual owning more than 25% of that entity. The EU’s 6AMLD and the US Beneficial Ownership Information (BOI) Reporting System both drive this requirement. Build a UBO capture module into your KYB onboarding flow early — retrofitting it after thousands of corporate accounts have already registered is painful.

Sumsub vs Veriff vs Jumio: Which Fits Your Platform

These three handle most enterprise-grade eKYC in fintech. Here’s how they compare for prediction market use cases specifically.

Sumsub is the strongest choice for document coverage and SDK flexibility. It supports 6,000+ document types across 220+ countries, offers passive liveness detection by default, and has a modular workflow builder you configure without custom code. Pricing runs about $1.50 to $2.50 per verification at standard volume tiers. For platforms targeting users in Southeast Asia, LATAM, or Sub-Saharan Africa, Sumsub’s document breadth is hard to match.

Veriff runs consent-based video verification. Conversion rates are slightly higher for EU users who recognize the brand, but the flow introduces more friction. If your audience skews European and GDPR-compliant data residency within the EU matters for your legal structure, Veriff has the right compliance infrastructure for that specifically.

Jumio is enterprise-grade. Expect $3 to $5 per verification, but its KYX product bundles identity verification and transaction risk scoring into a single API call. For high-volume US user bases above the Tier 2 deposit threshold, Jumio’s depth with FinCEN reporting workflows justifies the cost premium. It’s not the right choice for an early-stage platform with a tight budget, but it’s the right choice once you’re scaling compliance operations rather than just checking boxes.

All three support webhook callbacks, ship PHP and Node.js SDKs that integrate cleanly into a Laravel or Node microservices architecture, and offer sandbox environments for pre-launch testing. Run at least 200 simulated onboarding tests before going live — including edge cases like expired IDs, partial face matches, and unsupported document types from your target markets.

Frequently Asked Questions

Do decentralized prediction markets need KYC?

Yes, in most jurisdictions. The decentralized nature of the smart contract layer doesn’t exempt the platform operator from regulatory obligations. Polymarket operated as a decentralized platform and still paid a $1.4 million CFTC settlement for running without KYC controls. If you’re the legal operator or developer, KYC and AML obligations typically attach to you, not the smart contracts.

What’s the difference between CDD and EDD in a prediction market context?

Customer Due Diligence (CDD) is the standard verification process every user goes through — identity check, basic watchlist screening, risk score assignment. Enhanced Due Diligence (EDD) applies to high-risk accounts: PEPs, users from high-risk jurisdictions, corporate accounts, or anyone flagged by transaction monitoring. EDD involves additional documentation, source-of-funds verification, and quarterly re-verification rather than annual.

How do I handle KYC for non-US users?

Your KYC provider determines global coverage. Sumsub supports 220+ countries and 6,000+ document types, which covers most global user bases. The key distinction for non-US users is that AML rules vary by jurisdiction — EU users fall under AMLD6, UK users under MLR 2017, Singapore users under MAS AML/CFT guidelines. Your compliance stack needs jurisdiction-aware workflows, not a single global ruleset. Most modern KYC APIs support configurable jurisdiction-specific flows.

What AML rules should a prediction market configure at launch?

At minimum: a $10,000 single-deposit threshold alert, a 30-day cumulative deposit alert at $25,000, a structuring pattern detector watching for multiple deposits just under round numbers in a 7-day window, a high-velocity withdrawal alert triggered when a full account balance withdraws within 48 hours of a large win, and a cross-account device fingerprint cluster alert. Add custom rules based on your specific market types within the first 90 days of operation.

How does Travel Rule compliance affect user experience?

For most users it’s invisible. The VASP-to-VASP data transfer happens in the background. Users only see friction if their receiving wallet belongs to an unregistered VASP — at which point you add a documentation step before releasing funds. Expect about 5 to 8% of crypto withdrawals to trigger this prompt in early operations, dropping as your Travel Rule counterparty network expands.

Can I use a white-label KYC module instead of building my own?

Yes, and you should. Building KYC from scratch means maintaining document OCR models, liveness detection algorithms, watchlist feed subscriptions, and audit logging infrastructure yourself. White-label KYC modules from Sumsub, Veriff, or Jumio handle all of that. Your job is integrating their API and webhook callbacks into your compliance microservice — not rebuilding the verification stack.

What happens if my platform processes a transaction for a sanctioned user?

Depends on whether it was preventable. Willful or negligent processing of transactions for OFAC-sanctioned individuals carries civil penalties up to $356,000 per transaction, and criminal exposure if intent is demonstrated. The CFTC’s March 2026 announcement specifically flagged willful AML and KYC violations as a criminal referral priority. Your defense is your audit trail: timestamped OFAC screening results showing you ran checks at onboarding and on every transaction. No trail means no defense.